What Happens to Payroll Tax Debt When a Business Closes?

Closing a business does not automatically wipe out its payroll tax debts. The IRS will still expect those taxes to be paid, and it has tools to hold individuals personally responsible for the unpaid amounts. Payroll taxes (employment taxes withheld from employee wages) are considered “trust fund” taxes. This means the business was holding those funds on behalf of the government, so failing to remit them is taken very seriously. Even if companies go under, the IRS can and will pursue collection of payroll taxes from those responsible.

Many businesses encounter financial difficulties that result in unpaid payroll taxes and IRS enforcement actions, making this a common and serious issue for struggling companies.

In recent years (2024–2025), the IRS has maintained strict enforcement of payroll tax compliance. The IRS prioritizes payroll tax cases and aggressively tracks down unpaid employment taxes. Not only can it impose civil penalties, but egregious payroll tax violations sometimes lead to criminal prosecution. The bad news is that unresolved payroll tax penalties can result in significant challenges, including aggressive IRS collection tactics and personal liability for business owners. The bottom line is that shutting down your business won’t eliminate the payroll tax debt. In fact, the Trust Fund Recovery Penalty (TFRP) allows the IRS to go after owners and other responsible individuals personally to ensure these taxes are paid.

Payroll tax debts are generally not dischargeable in bankruptcy. So you can’t simply file bankruptcy to eliminate trust fund taxes. Before closing your business (or immediately after if you had to shut down abruptly), you should understand your exposure to these debts and take steps to resolve them. When a business falls behind on payroll tax obligations, the IRS may initiate enforcement actions, including liens, levies, and penalties, which can complicate the process of winding down the company.

Key Takeaways

- Payroll tax debt doesn’t vanish on business closure: These debts are especially troublesome because they typically cannot be discharged in bankruptcy and may follow responsible individuals even after the business is gone.

- Trust fund taxes are different: Payroll taxes are “trust fund” taxes – money withheld from employees (income tax and the employee portion of Social Security/Medicare) that the employer must remit. The IRS views failure to pay these as a serious breach of trust.

- Personal liability via TFRP: The IRS can hold individuals personally liable for unpaid trust fund taxes through the Trust Fund Recovery Penalty (TFRP). Any responsible person (not just the owner) who willfully fails to pay can be assessed a penalty equal to the unpaid tax. Once assessed, the IRS can file tax liens or issue levies against your personal assets to collect the debt.

- Address payroll taxes before closing: It’s best to resolve any outstanding payroll tax filings or payments before shutting down. If back taxes remain when the business closes, be proactive in working out a payment plan or other resolution with the IRS, rather than ignoring the debt.

Why Payroll Tax Debt Is Different

Payroll taxes are unlike most other business debts because of their trust fund nature. These taxes include employee withholding (for income tax, Social Security, and Medicare) and other employment taxes that the business holds in trust to pay to the IRS. Business taxes, including payroll and sales taxes, remain obligations even after a business closes and may result in penalties if unpaid. The same concept applies to certain state taxes, such as sales tax—the business is collecting money from customers on behalf of the state. Unpaid sales taxes are a solemn legal obligation, and sales taxes are a mandatory responsibility that cannot be avoided, even if the business is shut down. Failing to pay trust fund taxes is not only a debt issue but is also viewed by the IRS or state as effectively stealing from employees or customers. The government is very protective of these funds.

Unpaid payroll tax debt triggers specific consequences. The IRS will aggressively pursue trust fund taxes even if a business is closed or bankrupt. These debts are complicated to eliminate. For example, trust fund taxes are generally not dischargeable in bankruptcy proceedings. The law makes this clear: certain priority debts, such as withheld payroll taxes, remain your responsibility. In short, payroll tax debt persists, and the IRS gives it top priority in collections.

Personal Liability and the Trust Fund Recovery Penalty (TFRP)

For most tax debts of a business, only the business’s assets are at risk. Payroll taxes are distinct due to the Trust Fund Recovery Penalty (TFRP). Under Internal Revenue Code § 6672, the IRS can assess a penalty equal to 100% of the unpaid trust fund taxes against any responsible person who willfully failed to collect or pay those taxes. In essence, the TFRP lets the IRS reach into your personal finances to collect the tax that wasn’t paid by the business.

Who can be held responsible? It’s not limited to the business owner. A “responsible person” is anyone with sufficient duty and authority over the business’s finances or tax payments. This can include people like:

- Owners and corporate officers (e.g., CEOs, presidents)

- Partners or LLC members

- Managers and supervisors who direct financial decisions

- Bookkeepers or accountants handling payroll/tax deposits

- Treasurers, controllers, or comptrollers

- Payroll service providers or third-party payers in charge of taxes

In determining responsibility, the IRS considers who had control over finances and decision-making power regarding the payment (or non-payment) of taxes. Willfulness means that the person knew (or should have known) about the unpaid taxes and chose not to pay, or was plainly indifferent to the obligation. Importantly, even employees who aren’t owners can be liable if they had significant responsibility and willfully failed to ensure the taxes were paid. On the other hand, someone with no absolute authority (for example, a junior employee who follows orders) typically wouldn’t be considered a responsible person.

If the IRS successfully assesses the TFRP against you, you now owe that amount personally. The IRS will send a bill, and from there, it can take collection action, such as filing a federal tax lien on your property or issuing levies (for instance, garnishing your wages or seizing bank accounts) to collect the debt. In severe cases of payroll tax evasion, the IRS may also pursue criminal charges, but even civil TFRP consequences are severe for your finances.

How the IRS Assesses the TFRP (Investigation and Notice)

When a business has unpaid payroll taxes, the IRS often assigns a Revenue Officer to investigate and determine who should be personally assessed with the trust fund penalty. The process typically involves an interview and a formal notice:

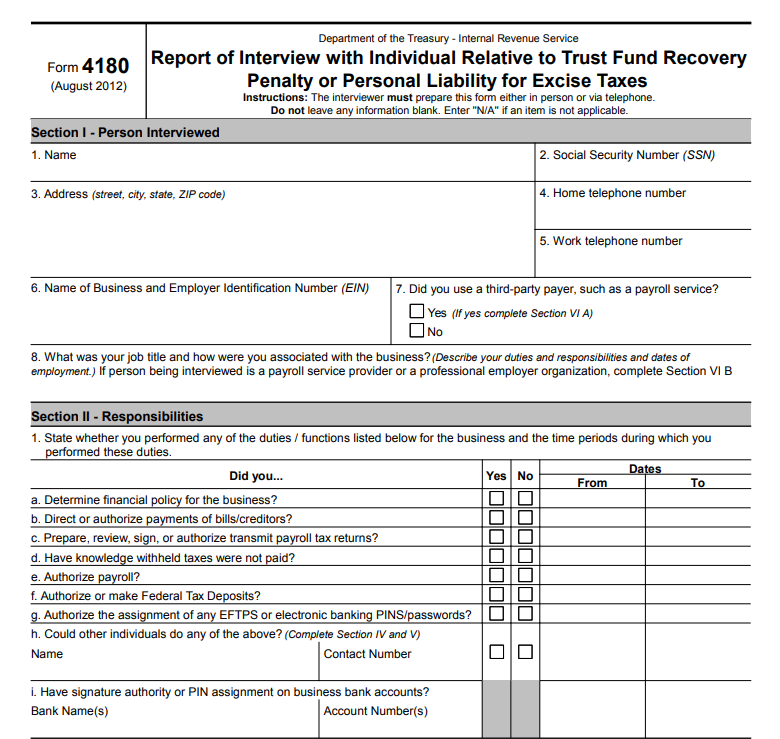

Form 4180 Interview

The IRS revenue officer will conduct interviews with key people involved in the business (often using IRS Form 4180 as a guide for questions). They ask about who was responsible for withholding and paying payroll taxes, who had check-signing authority, how the accounting system worked, and so on. The purpose is to identify all individuals who might meet the “responsible and willful” criteria for the TFRP. If you are involved in a business with payroll tax issues, you might be asked to participate in such an interview. It’s essentially your chance to explain your role and possibly demonstrate that you were not the willful responsible party.

Letter 1153 (Proposed Penalty Notice):

After the investigation, the IRS will decide who to hold personally liable. Those individuals will receive an IRS Letter 1153, which is a notice that the IRS intends to assess the Trust Fund Recovery Penalty against them. If you receive Letter 1153, do not panic. It’s not a final judgment, but it’s a severe warning. You generally have 60 days (or 75 days if the letter is addressed to you abroad) to formally appeal the proposed TFRP assessment. The letter is accompanied by Form 2751, which you can sign to agree to the evaluation if you choose not to contest it. If you agree and sign, the IRS will assess the penalty and send a bill. If you disagree, you can file a written protest or appeal within the 60-day window.

Take Action if You Get a Letter 1153

It’s highly advisable to consult a tax attorney or qualified professional at this point. You’ll need to decide whether to appeal or negotiate, and a professional can help present evidence that you weren’t responsible or didn’t act willfully, if that’s the case. Keep in mind that the IRS sometimes sends Letter 1153 to multiple individuals involved, even if they’re not 100% certain that all are truly liable. So, getting the letter doesn’t automatically mean you will end up owing—you have the right to defend yourself. The key is to respond within the deadline. If you ignore the letter and take no action, the IRS will assess the penalty by default and then proceed to collect it from you personally.

Steps to Close a Business With Unpaid Payroll Taxes

If you’re in the process of shutting down a business that still has payroll tax obligations, there are specific steps you should take to close out and minimize troubles properly:

File All Final Tax Returns

Ensure all required employment tax returns are filed, even if you can’t pay the full amount. For example, file your final IRS Form 941 (Quarterly Payroll Tax Return), Form 940 (annual unemployment tax), and any state payroll tax returns. This document outlines the liabilities and demonstrates good-faith compliance. Be sure to accurately report all final business income, as this affects your tax obligations and is necessary for resolving any outstanding tax debts.

Notify the IRS Personnel Involved

If a revenue officer or any IRS agent is already working your case, inform them that the business is closing. Open communication may help as they consider collection options or more lenient resolutions, knowing the business assets are gone.

Organize Records and Responsible Party Information

Keep a careful archive of your business’s records, primarily documents that show who was responsible for financial decisions and tax payments in the company. This can be crucial if there’s a later dispute about TFRP liability—for instance, to prove that specific individuals (perhaps you) were not in charge of payroll decisions during the period of nonpayment.

Address Any TFRP Actions

If the IRS has already assessed a TFRP or is in the process of doing so, be sure to appeal or respond as necessary. Closing the business doesn’t halt that process. You may need to fight the penalty or work out payment arrangements for it. Remember, the IRS will attack your personal assets, especially when it can no longer collect from the business.

Address All Outstanding Debts

It’s essential to address all outstanding debts—not just payroll taxes—when closing your business. This includes loans, vendor bills, and other liabilities.

Understand Asset Seizure and Remaining Balances

If the IRS or other creditors pursue collection, they may consider seizing business assets such as bank accounts, inventory, equipment, or property. This is typically a last resort after other collection efforts have failed, but the IRS can and will do so if necessary. The process of seizing and selling business assets can be very time-consuming for both the IRS and the business owner. If the sale of assets does not cover the full amount owed, creditors and the IRS may still pursue any remaining debts.

Options for Settling Payroll Tax Debts

Ultimately, payroll taxes (and any associated TFRP assessments) will need to be repaid; however, the IRS provides various resolution options if you cannot pay in full immediately. Depending on your tax situation, you or the now-closed business might pursue one of the following:

Installment Agreement (Payment Plan): This is an arrangement that allows you to pay the taxes over time in monthly installments. The IRS often will enable businesses or individuals to pay back payroll taxes in installments if full payment upfront isn’t feasible.

Offer in Compromise (OIC): An OIC is a settlement offer to pay less than the full amount owed if you can prove you are unable to pay the full debt. If the business settles via an OIC, it doesn’t eliminate personal responsibility for the debt (unless the settle includes full payment of the trust fund)

Partial Payment Installment Agreement (PPIA): This is a hybrid arrangement where you pay installments over time, but not the full debt amount, and the remaining balance may be forgiven if the statute of limitations expires. It’s like a long-term hardship plan. It’s more challenging to obtain, but it may be an option in certain instances.

Currently Not Collectible (CNC) Status: If neither the business nor you (as a responsible individual) can pay anything, the IRS can designate the account as “currently not collectible.” This pauses collection efforts. Interest and penalties still accrue, and it’s not a permanent fix, but it can buy time until your financial situation improves.

Please keep in mind that which option is the best path (and which the IRS will accept) depends on your specific facts. For example, an Offer in Compromise to settle payroll taxes might only be considered if the business assets are gone and the individuals responsible have limited ability to pay.

Negotiating with the IRS to settle your tax bill can help you avoid asset seizures and improve your overall tax situation. Before deciding on a strategy, it’s best to consult with a tax professional who can analyze your financial situation and the nature of the tax debt to recommend the most viable solution. A professional can help you determine the best path forward for resolving payroll tax debts.

If you need assistance with resolving payroll tax debt, please don’t hesitate to contact us today for a complimentary consultation.

Don’t Ignore Payroll Tax Debt – Get Professional Help

Unpaid payroll taxes are a top priority for the IRS, and ceasing your business operations will not prevent the IRS from enforcing collection. In some cases, closing a business can even prompt the IRS to move swiftly to assess penalties against individuals while they can. If your company is dissolving and you owe payroll taxes, it is essential to take action to protect yourself. This often means working out a deal with the IRS or defending yourself against a proposed TFRP.

Remember, the government has powerful tools at its disposal – from tax liens on your property to levies on bank accounts or wages – to ensure these debts are paid. The Trust Fund Recovery Penalty can tag you personally with what the business owes, so it’s not something to take lightly or handle casually.

If you’re in this situation, consider getting advice from a qualified tax attorney or tax resolution firm. Professional help can make a big difference in navigating IRS procedures and finding a manageable solution. At Paladini Law, for example, we regularly assist small business owners and responsible individuals with payroll tax problems. We can evaluate your specific circumstances, help you communicate effectively with the IRS, and work to prevent or minimize collection actions against you and your assets.

Closing a business is stressful enough—you don’t want lingering payroll tax debts to become a long-term personal nightmare. By addressing the issue head-on and seeking guidance, you can close your business with a clear plan for resolving the tax debt and move forward to a fresh start.