You opened the mail and found IRS Form 9297, the Summary of Taxpayer Contact. That single page means an IRS revenue officer has been personally assigned to your case. It’s no longer just the Automated Collection System sending you balance-due letters. A collection employee—an individual revenue officer—is now contacting you directly to collect payment on unpaid taxes.

This guide explains the form in plain English, walks you through the IRS collection process once a case is personally assigned, and provides a step-by-step plan to respond effectively. You’ll see what documents are usually requested, the timeline you should expect, how federal tax liens and levies fit in, what happens if a taxpayer fails to answer, and how an authorized representative (like a tax attorney) can handle the initial interview and negotiate a practical resolution.

What Is IRS Form 9297?

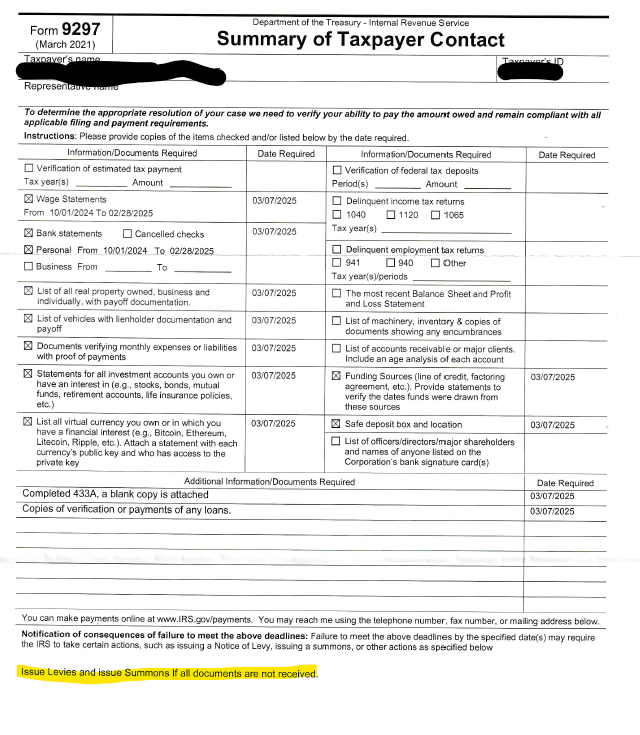

IRS Form 9297 is titled Summary of Taxpayer Contact. Think of it as the principal document the revenue officer uses to formalize a written request for information and set deadlines. When you receive IRS Form 9297, your case has moved beyond automated notices into a hands-on investigation by an IRS revenue officer who is personally involved.

Form 9297 is not a bill. It’s a written request with a due date. It identifies:

- The collection employee’s name and contact information

- The tax periods and type of tax liability involved (for example, individual income tax or payroll taxes)

- A list of financial documents and unfiled tax returns that the revenue officer needs

- A response due date and instructions for mailing form responses or submitting via secure channels

- Next enforcement steps if you do not respond

Because this is an IRS form used by field collections, it’s a serious escalation in the IRS collection process. Treat it as an opportunity to demonstrate good faith, establish effective communication, and steer the case toward a solution before enforcement escalates.

Why You Received Form 9297

Cases are routed to a revenue officer when certain risk or complexity indicators are present. Common triggers include:

- Multiple delinquent returns or unfiled tax returns (sometimes several years)

- A large tax balance or repeated back taxes that have grown with penalties and interest

- Prior ignored IRS letter notices from the Automated Collection System

- Business accounts with payroll taxes, potential trust fund recovery penalty exposure, or ongoing compliance issues

- Indicators that field contact is needed to verify payments, assets, or the ability to collect payments

Bottom line: the IRS believes personal, phone-based contact or outgoing face-to-face contact is required to resolve your tax issues. A revenue officer may reach out to you at your home, business, or by phone to initiate the initial interview and outline the next steps.

What the Form Usually Requests

Every case is different, but most Form 9297 packages request a collection information statement and supporting financial documents so the IRS can evaluate your ability to pay. Expect some or all of the following:

- Form 433-A (collection information statement for wage earners/self-employed)

- Form 433-B (collection information statement for businesses)

- Form 433-F (streamlined financial form used by ACS—sometimes a revenue officer will accept it; often they won’t)

- Bank statements (personal and business bank statements) for the most recent 3–6 months

- Pay stubs or other proof of income (the most recent pay stub or recent pay stub set, typically 3 months)

- Proof of other income sources (contract income, rental income, dividends)

- Mortgage statements, lease agreements, and recent utility bills

- Vehicle notes, titles, and insurance statements

- Investment assets and retirement statements

- Asset and liability lists, including personal assets that the IRS may consider in equity analysis

- Unfiled returns or delinquent returns the IRS wants immediately

- Employer Identification Number (for business entities) and responsible party details

These requests provide the IRS with a comprehensive picture of your financial accounts, income sources, and necessary living expenses. The revenue officer uses this financial information to recommend a resolution—an installment agreement, a short-term full payment plan, a partial payment option, currently non-collectible status, or, where appropriate, referral for an Offer in Compromise.

The Role of the IRS Revenue Officer

A revenue officer is a field collections professional trained to investigate, secure delinquent returns, analyze collection information statements, and collect payments. Unlike generic IRS employees you might reach in a call center, a revenue officer may visit your business, review books and records, and interview household members or business partners to verify the tax situation.

Key powers and tasks of a revenue officer include:

- Contacting taxpayers to secure unfiled returns and current compliance

- Analyzing financial form submissions and bank statements

- Recommending federal tax liens where appropriate

- Initiating levy action on wages or financial accounts if the taxpayer fails to cooperate

- Considering penalty abatement requests and verifying reasonable cause facts

- Pursuing the trust fund recovery penalty against legally responsible persons in payroll tax cases

- Issuing a formal summons to you or third parties if documents are not provided

- Closing cases with an installment agreement, currently non-collectible status, or referral for an offer in compromise

While a revenue officer may be firm, the best results usually come when you demonstrate good faith and communicate through an authorized representative who understands representative conduct and the collection process.

ACS vs. Field Collections: Why This Letter Feels Different

Before a case is assigned to a field collections officer, most accounts begin with the Automated Collection System. ACS sends standardized notices, may set up a basic payment plan, and will file system-triggered liens or levy certain assets if you ignore an IRS letter. Once the account is identified as having higher risk, complexity, or non-responsiveness, it can be personally assigned to a revenue officer.

Key differences:

- ACS often accepts a streamlined installment agreement based on limited questions; a revenue officer typically requires a full collection information statement with documentation.

- ACS is phone-driven; a revenue officer may schedule an initial interview in person or by phone and can request books and records.

- ACS actions are rules-based; a revenue officer can tailor deadlines, request specific financial documents, and escalate the matter more quickly if a taxpayer fails to respond.

Put simply, IRS Form 9297 is your notice that a human is now steering your case—and that personal accountability has entered the picture.

How Fast You Must Respond

Form 9297 usually sets a short deadline—often 10 to 14 days from the date of the written request. That clock is tight, and mailing form responses can eat into your time. If you cannot gather everything by the due date:

- Contact the revenue officer before the deadline.

- Show good faith by submitting partial information (for example, send the completed Form 433 and the first batch of bank statements).

- Request a specific, reasonable extension and clearly outline what is outstanding, along with the expected completion date.

Silence is treated as non-cooperation. A simple, timely email or call can help preserve trust and prevent enforcement action.

What Happens If You Ignore Form 9297

If a taxpayer fails to respond, the revenue officer may:

- Issue a formal summons to you (or third parties) for the documents.

- Recommend or file federal tax liens, affecting financing options and property transfers.

- Initiate wage garnishment or levy action against bank accounts and other financial accounts.

- Visit your business location and conduct an in-person interview.

- Pursue the trust fund recovery penalty against responsible persons for payroll taxes.

- Recommend seizure in limited, serious cases.

Enforcement is not automatic on day one—but the runway is short. Responding promptly and completely is the only reliable way to avoid escalation.

How To Respond Effectively

Follow this sequence to keep control of the process.

Step 1: Read the Entire Notice

Confirm the tax periods, the exact documents requested, and the due date. Note the revenue officer’s name, phone number, and email at the IRS office handling your case.

Step 2: Get Representation

If possible, seek representation. While there are plenty of times when you can handle tax debt yourself (such as when the matter is with ACS), this is not one of them. An authorized representative, such as a tax attorney, can file Form 2848, speak directly with the officer, and ensure that your financial information is accurate and complete without over-sharing. When you seek representation, you reduce the risk of saying something that complicates the case.

Step 3: Gather Financial Documents

Start with the list on the form and add the following:

- Collection information statement (Form 433-A or 433-B) completed and signed.

- Pay stubs for the last 3 months (or most recent pay stub if that’s all you have on hand, followed by the rest quickly).

- Bank statements (personal and business bank statements) for the requested period.

- Mortgage, rent, and recent utility statements.

- Proof of insurance, transportation, and other necessary living expenses.

- Investment assets and retirement account statements.

- Copies of any delinquent returns that you file immediately.

Organize everything by category with clear, labeled sections. This demonstrates good faith and helps the officer verify payments and expenses faster. The easier you make their job, the more they’ll like you. The more they like you, the better results you get.

Step 4: Fix Missing Filings

If you have delinquent returns, file them right away. Getting current is non-negotiable for tax resolution options. A taxpayer who files now shows the IRS that ongoing compliance is a priority.

Step 5: Propose a Resolution

Don’t just submit paperwork—propose a plan:

- Installment agreement or installment plan with a realistic monthly payment.

- Partial payment plan if your budget won’t support full amortization.

- Offer in Compromise if severe hardship exists.

- Currently non-collectible status if you cannot pay after basic expenses.

Tie your proposal to the numbers in your collection information statement. When your plan aligns with the documented budget, it becomes easier for the officer to approve.

Step 6: Stay Current Going Forward

While negotiating, keep current with estimated tax payments (if required) and withholding. Ongoing compliance is part of every approval. Falling behind while you’re in negotiations signals risk and can derail an agreement.

Special Considerations for Businesses and Payroll Taxes

Business cases—especially those involving payroll taxes—receive heightened attention. If the business owes trust fund taxes (the employee portion of withheld payroll taxes), the IRS can assess the trust fund recovery penalty against individuals who were legally responsible and willfully failed to deposit. That can include owners, officers, or anyone with authority over the business bank account or payroll process.

What the revenue officer may request:

- Business bank statements and merchant statements

- Payroll tax returns (Forms 941/940) and deposit histories

- Responsible party details (including titles and authority)

- Books, ledgers, and proof of where funds went during the delinquency

If you’re not solely responsible, clarify roles. Document who controlled disbursements, signed checks, and had the final say. This can limit personal exposure and help the officer distinguish between owners and employees.

Understanding Federal Tax Liens and Levies

A federal tax lien is a legal claim against all your property and rights to property when a tax is assessed and not paid after notice and demand. It attaches broadly—to real estate, vehicles, accounts, and future rights. The IRS may file a Notice of Federal Tax Lien to protect its claim and alert creditors.

A levy is different—it’s the taking action: seizing funds from bank accounts, garnishing wages, or taking other property. Form 9297 itself is not a lien or levy. But if you do not respond, federal tax liens and levies are the predictable next steps.

How to reduce levy risk:

- Respond on time.

- Use a direct debit installment agreement when possible to avoid defaults.

- Keep current with filing and deposits.

The Initial Interview

Whether by phone-based contact or in person, the initial interview sets the tone. Expect questions about:

- Household members and dependents

- Employment, business operations, and other income

- Necessary expenses vs. discretionary costs

- Assets with equity (vehicles, real estate, investment assets)

- Prior attempts to set up a payment plan or resolve the tax balance

- Any recent large transactions or transfers of personal assets

Be truthful and concise. If the officer asks something you don’t understand, ask for clarification. It’s fine to ask for time to gather exact figures rather than guessing. Pro tip: Hire a tax attorney to handle this interview for you. You don’t even need to speak to the revenue officer if you have representation!

Frequently Used Forms and What They Mean

- Form 9297: Summary of Taxpayer Contact—the written request and deadline

- Form 433-A/B/F: Collection information statements—your financial snapshot

- Form 2848: Power of Attorney—allows your representative to speak for you

- Form 433-D: Installment agreement request—used to formalize a payment plan

- Form 656 with 433-A(OIC)/433-B(OIC): Offer in Compromise package

Each IRS form supports a step in the collection process. Completing the proper form fully and accurately is more important than rushing every form at once.

Common Mistakes To Avoid

- Ignoring the deadline or sending nothing.

- Submitting partial financial information without explanation.

- Proposing a payment you can’t sustain to “get them off your back”.

- Failing to make current estimated tax payments while negotiating.

- Over-sharing documents that aren’t requested and creates new questions.

- Assuming the revenue officer will accept verbal summaries instead of documents.

- Waiting until levy action begins to seek representation.

The antidote to every mistake above is the same: communicate early, demonstrate good faith, and submit organized, accurate financial information.

Resolution Paths: Matching Your Tax Situation To The Right Option

- Short-term full payment: If you can pay in 120 days, ask for time to liquidate assets or move funds. This can avoid a payment plan entirely.

- Installment agreement: The most common option; aim for a direct debit setup.

- Partial payment installment agreement: When the numbers don’t support full amortization, propose a smaller sustainable payment backed by your 433.

- Offer in Compromise: Reserved for significant hardship. Be ready with detailed financial disclosures.

- Currently non-collectible status: When there’s no ability to pay after necessary living costs, CNC can pause enforcement while you stabilize.

Choosing the right path—and documenting it—often determines whether your proposal is accepted.

A Practical Timeline After Form 9297 Arrives

Week 1

- Read the form, calendar the deadline, and contact a tax professional.

- Request transcripts and gather the most recent pay stub(s), bank statements, and bills.

Week 2

- File delinquent returns.

- Complete your collection information statement and assemble supporting financial documents.

Week 3

- Submit a complete, organized package with a written request for your preferred resolution (installment agreement, etc.).

- If you need more time for a few items, explain what’s missing and the date you will deliver it.

Week 4 and beyond

- Answer follow-up questions quickly.

- If approved, sign the installment agreement and keep up with timely payments.

- Stay current on all new-year tax obligations to avoid default.

Penalties, Abatement, and Compliance

While you’re resolving the balance, ask whether penalty abatement is appropriate. If you have reasonable cause (serious illness, disaster, reliance on erroneous professional advice) or qualify for first-time abatement, a portion of the penalties may be reduced. Continued compliance (timely filings and payments) strengthens both abatement arguments and payment plan requests.

When a Summons Appears

If you don’t respond—or your response is incomplete and you refuse to cooperate—the revenue officer may issue a formal summons. A summons compels production of records or testimony. Ignoring it can lead to court enforcement. If you receive one, seek representation immediately.

What To Do If You Disagree With The Liability

Form 9297 is about collection, not litigation over whether the tax is correct. But if the tax liability is wrong—wrong return filed, identity theft, missing credits—tell your representative. Options can include audit reconsideration, amended returns, appeals, or other corrective processes. You can pursue liability fixes while still proposing a payment plan to pause enforcement.

Your Rights During Collection

Even while the IRS collects, you have rights:

- The right to be informed and to receive clear explanations.

- The right to quality service from IRS employees.

- The right to pay no more than the correct amount of tax.

- The right to challenge the IRS’s position and be heard.

- The right to appeal certain collection actions.

- The right to finality, privacy, and a fair collection process.

- The right to retain representation.

Knowing your rights helps you push back respectfully if requests drift beyond what’s needed to resolve the case.

Why Work With a Tax Attorney

A seasoned tax attorney:

- Screens your facts for the best tax resolution options

- Builds accurate 433 financials and avoids over-sharing

- Coordinates the initial interview and ongoing communications

- Acts as a buffer between you and the IRS

- Negotiates a payment plan you can maintain

- Helps address payroll tax and trust fund recovery penalty exposure

- Watches deadlines and keeps you compliant so you don’t default

If you’re overwhelmed or not sure where to start, seek representation before the deadline. A quick free consultation can clarify your next steps and prevent errors that lead to levy action.

How Paladini Law Helps

Review and strategy

We review IRS form 9297, identify what the revenue officer truly needs, and map a strategy to demonstrate good faith without volunteering unnecessary information.

Communicate for you

We become your point of contact, allowing the revenue officer to work through us. That reduces stress and ensures consistent, accurate responses.

Prepare the financial package

We complete the collection information statement, assemble bank statements, pay stubs, and supporting financial documents, and present a clean, well-supported request.

Negotiate resolution

We propose the right plan—installment agreement, partial payment, offer in compromise, or currently non-collectible—based on your verified budget. We also pursue penalty abatement where appropriate.

Protect against enforcement

If a levy or wage garnishment is threatened, we work to stop it, demonstrating good faith and a viable alternative so collection can proceed cooperatively.